If you’re trying to decide between leasing and buying your next business vehicle, one question is probably foremost in your mind:

Which option costs less?

Unfortunately, comparing the costs of leasing and buying isn’t as simple as it looks. To do it right, you must consider not just out-of-pocket costs but also

-

- cash available,

- the tax benefits of each option, and

- the time value of money.

The Difference between Lease and Buy . . .

When you buy, you own the vehicle free and clear after you repay the loan. So you get the trade-in or sale value of the vehicle when you decide to get rid of it.

When you lease, the dealer or leasing company owns the vehicle, and you pay for its use over the lease term. When the lease ends, you can either buy the vehicle for a “residual value” stated in the lease or walk away and get a new vehicle.

. . . and the Impact on the Cost Calculation

Leasing requires less money up front and often lower monthly payments. Consequently, leasing leaves you more cash. That’s an advantage you must account for in your cost calculation.

Another key factor in the comparison is how much you can save on taxes using each option. The key tax differences could involve bonus depreciation, Section 179 expensing, and MACRS depreciation.

Buy

If you buy your vehicle and use the vehicle in your business, you can deduct the cost of operating and maintaining it using either

-

- a pre-determined mileage rate set by the IRS (which for 2024 is 67 cents per mile, and that 67 cents includes 30 cents for depreciation),1 or

- your actual expenses (operating expenses plus depreciation and Section 179 expensing).2

Key point. The actual expense method gives you your deductions quicker than the mileage method because, depending on the type of vehicle, you can claim the following:

-

- Bonus depreciation

- Section 179 expensing

- MACRS depreciation

Lease

You can also use the mileage rate or actual costs to deduct vehicles you lease. The actual cost deduction for business vehicles you lease consists of

1. monthly lease payments,

2. amortization of down payment and other up-front costs, and

3. lease reduction amounts for luxury vehicles, if applicable.

The Gnat’s Whisker

How can you absolutely know whether it’s better to buy or lease? Easy. Just use the After-Tax Adjusted

Present Value Lease Calculator. It resides in your subscriber resources, but don’t go there now. We’ll give you the link later in this article, after we explain how this works and why it’s superior.

For now, you can relax knowing that you have us to make all the present value (PV) and tax calculations for you. When you click the link and get to the calculator, you simply enter your buy and lease numbers.

The After-Tax Adjusted Present Value Method

The after-tax adjusted present value method takes the money you pay out and the money you collect and values that money in today’s dollars so you can make a true comparison.

To value the money, you start with this question: what is your safe rate of investment return after taxes? With that number, the calculator values the cash intake and outlay and makes the comparison. It works like this:

|

Buy |

The calculator uses your numbers to find the net after-tax cost in today’s dollars to buy the vehicle by finding the PV of the purchase, sale, tax benefits, and detriments. |

|

Lease |

The calculator uses your numbers to find the net after-tax cost in today’s dollars to lease the vehicle by finding the PV of the cash outlays, tax savings, and add-backs. |

The Formula

Let’s say you are looking at a four-year period of ownership for a new car and you are comparing buy versus lease.

You enter your numbers in a template and the calculator crunches the numbers. The results below look a little scary, but remember, you are not doing the math—the calculator does the math.

Here’s what the calculator is going to show you, if you want the details:

PV If You Buy

| Cash paid at purchase | Add |

| PV of total monthly payments to buy the vehicle, if financed | Add |

| PV of tax savings from interest deductions | Subtract |

| PV of tax savings from depreciation | Subtract |

| PV of expected cash from sale of the vehicle | Subtract |

| PV of tax benefit if sold at a loss, or tax detriment if sold at a profit | Add or subtract |

| After-tax adjusted present-value cost to buy the vehicle and use it in business | Total of above |

PV If You Lease

| Cash paid at lease signing | Add |

| PV of monthly lease payments, excluding first and last month | Add |

| PV of security deposit returned at the end of the lease | Subtract |

| PV of tax savings from monthly lease payments | Subtract |

| Tax savings from first month’s lease payment | Subtract |

| PV of tax savings from last month’s lease payment | Subtract |

| PV of tax savings from amortization of lease payment reductions and lease acquisition | Subtract |

| PV of tax effect from tax detriment lease inclusion amounts | Add |

| PV of payments due at the end of the lease term to walk away from the vehicle | Subtract |

| PV of tax savings from walk-away payment | Add |

| After-tax adjusted present-value cost to lease the vehicle and use it in business | Total of above |

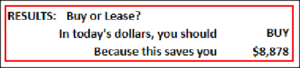

Key point. You enter the numbers such as the cost of the vehicle, down payment, lease payments, etc., in the calculator and the calculator generates all the information above—the details. And from those details, the calculator gives you the results, which look like this:

Three key points here:

1. You enter the numbers—it’s easy.

2. The calculator crunches the numbers.

3. You see the result—it’s an after-tax result in today’s dollars (the PV).

It’s Not All about Money

When you use the After-Tax Adjusted Present Value Lease Calculator, you get to the real cost difference between buying and leasing. To use the calculator, click here.

Although cost is important, keep in mind that there are also personal factors you need to consider in deciding between lease and buy, such as these:

-

- How often you want a new vehicle—leasing gives you a big push to get a new vehicle every three years or so, when the lease ends.

- How much you trust the dealer or other lessor—leasing is a more complex transaction that requires closer contact with and more dependence on the dealer or other lessor.

- How much you drive—leased vehicles are subject to mileage limits as well as fees for excess damage, which may be a major bummer if you plan to drive the vehicle a lot and treat it roughly.

- The stability of your personal life—you may be much better off not being hemmed in by a lease if you’re not sure what your family or business situation will be in a couple of years.

- Status considerations—because leasing costs are generally lower, you can lease a vehicle that you couldn’t afford to buy.

Takeaways

When deciding whether to buy or lease a business vehicle, consider these key points for a balanced understanding.

Up-front and ongoing costs:

-

- Leasing often requires less initial cash and has lower monthly payments, enhancing cash flow.

- Buying, though costlier up front, leads to vehicle ownership and potential resale value.

Tax considerations. Both options offer tax advantages. Buying allows quicker deductions because of bonus depreciation and possible Section 179 deductions.

If you want to know the difference between leasing versus buying in today’s dollars, use the After-Tax Adjusted Present Value Calculator. It compares the financial impact of buying versus leasing by evaluating present and future costs and benefits.

Personal and business needs. Your decision should factor in how often you prefer a new vehicle, your driving patterns, and the stability of your personal or business life. Leasing may demand closer ties with dealers or other lessors and can impose mileage limits.

1. IRS Notice 2024-8.

2. Rev. Proc. 2019-46.