It’s Not Too Late: Qualify Now for Your 2020 and 2021 ERC Money

Okay, it’s 2023. But it’s not too late to qualify for the employee retention credit (ERC).

If you qualify and want your money, you must amend your 2020 and 2021 payroll tax returns.1 Sure, that’s a pain.

But if you have a dozen employees and qualify for maximum tax credits, you are looking at $312,000.2 That certainly nullifies the minor pain of amending those payroll tax returns.

Oh, you’ll also need to amend the business income tax returns for 2020 and 2021 to show the ERC as a reduction in payroll expenses for the qualifying years.3 Again, not hard—just a pain.

How Do I Qualify?

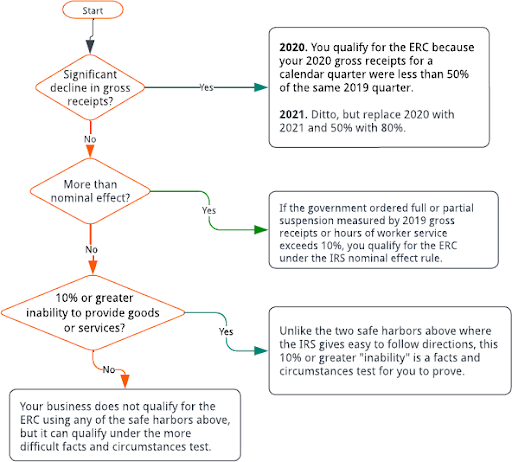

Assuming you aggregated your businesses and paid qualified wages in 2020 and 2021, look at the following flowchart for the big picture on how you can qualify for the ERC.

Decline in Gross Receipts

Decline in Gross Receipts

The gross receipts test is mechanical. COVID-19 did not have to cause your decline in gross receipts.

Key point. The gross receipts test renders the maximum ERC money because it applies to the entire quarter, whereas ERC full or partial government suspension money comes from only the days you were affected by the local, state, or federal shutdown or suspension order.

2020 Decline in Gross Receipts

You qualify for the 2020 ERC of up to $5,000 per employee when4

- your 2020 quarterly gross receipts are less than 50 percent of your gross receipts for the same calendar quarter in 2019, and

- your gross receipts in the 2020 quarter that follows the 2020 quarter described above (i.e., the less-than- 50 percent quarter) are less than 80 percent of your gross receipts for the same calendar quarter in 2019.

2020 gross receipts example 1. Your 2020 quarter 2 gross receipts are 43 percent of your 2019 quarter 2 receipts. Your wages paid during quarter 2 qualify for the ERC.

2020 gross receipts example 2. Your 2020 quarter 3 gross receipts are 73 percent of your 2019 quarter 3 gross receipts. Under the lookback rule where quarter 2 receipts were less than 50 percent, your quarter 3 wages qualify for the ERC.

2021 Decline in Gross Receipts

The 2021 ERC is available for quarters one, two, and three for up to $7,000 per eligible employee per quarter. That’s

$21,000 of possible ERC per employee compared with $5,000 in 2020.

To qualify under the gross receipts test, you compare 2021 calendar quarter gross receipts with the same quarter of 2019. If the 2021 gross receipts are less than 80 percent of the 2019 gross receipts for the same quarter, you qualify for that quarter.5

2021 gross receipts example 1. Your gross receipts for quarter 2 of 2021 are 75 percent of your gross receipts for quarter 2 of 2019. Your wages paid during quarter 2 qualify for the ERC.

Lookback bonus. When you look at the gross receipts test for a 2021 calendar quarter and you don’t qualify for that quarter, you could still qualify for the ERC under the “election to use the alternate quarter” rule.6

Under this 2021 rule, you look back to the prior month. If you qualified in the prior month, you qualify in the current month. When looking at quarter 1 of 2021, your lookback month for the 80 percent qualification is December 2020.7 (Note. This is a 2021 lookback and has no effect on your 2020 calculations.)

Gross receipts example 2. Your gross receipts for quarter 3 of 2021 are 117 percent better than your gross receipts for quarter 3 of 2019. No problem. You qualify for the ERC under the alternative test that allows you to compare quarter 2, where you had the 75 percent result.8 Thus, your wages paid during quarter 3 qualify for the ERC because of quarter 2.

Government Order Causes More Than a Nominal Effect

If you don’t qualify for the ERC under the most favorable gross receipts rules discussed above, you may qualify because of a government full or partial shutdown order.

You likely have no trouble identifying a full or partial shutdown caused by a federal, state, or local government order. One thing to remember, as we mentioned before: when you qualify for the ERC under the full or partial shutdown, you earn the ERC only for wages paid during the shutdown period.9

To determine whether your business suffered a partial suspension of operations from a government order, you need to have had more than a nominal portion of your business suspended. The question: What is a “nominal portion”?

Say thanks to the IRS. Rather than rely on facts and circumstances (which you can do), rely on the IRS safe-harbor 10 percent definition of “nominal portion.” (Note the magic words: “safe harbor.”)

It works like this.

The effect of the government order is deemed to constitute more than a nominal portion of your business operations if either10

- the gross receipts from that portion of the business operations are not less than 10 percent of the total gross receipts (both determined using the gross receipts for the same calendar quarter in 2019), or

- the hours of service performed by employees in that portion of the business are not less than 10 percent of the total number of hours of service performed by all employees in the employer’s business (both

determined using the number of hours of service performed by employees in the same calendar quarter in 2019).

For the time that you meet either the gross-receipts or worker-hours test, the IRS deems via its safe harbor that you suffered a more-than-nominal effect on your business operations and thus you qualify for the ERC during that time period.

Example. A 2020 government order required Sam to shut down his bar and restaurant to sit-down service for 61 days of quarter 2. Sam looks at his 2019 second-quarter results and finds that his sit-down service was 73 percent of his gross receipts for that 2019 quarter. During the 61 days that Sam was shut down by this government order, he qualifies for the ERC.11

Sam also could look at 2019 worker hours rather than gross receipts for that quarter. For example, say Sam had 75 employees, and 50 worked in the bar and restaurant’s sit-down service. Under this circumstance, Sam qualifies for the ERC for the 61 days that the government order was in effect.

Key point. Sam has the two possible ways to qualify for the nominal-effect safe harbor: (a) gross receipts and (b) hours of worker service. He does not need to meet both requirements—just one. And he can pick the more favorable one.

The IRS nominal-effect safe harbor for a full or partial shutdown is about a physical space change measured by 2019 numbers. You can also qualify for the ERC under your specific facts and circumstances or if the government order caused a modification to your business impeding your ability to provide goods and services.

Inability to Provide Goods and Services

Unlike the partial-shutdown option, where you can identify affected operations by physical space, the 10 percent “inability to provide goods or services” safe harbor requires facts and circumstances, good judgment, and likely some type of spreadsheet supported by proof.

Key point. The IRS deems that you qualify for the ERC when the local, state, or federal government order reduces your ability to provide goods or services in the normal course of your business by not less than 10 percent.12

Here are two situations where inability to provide goods and services could come into play during the time you were shut down:

- The government order limited your use of the physical space (e.g., keeping people and tables six feet apart).

- The government order limited the size of gatherings, which affected your business (e.g., no more than 10 people in the store simultaneously).

Example. Linda’s restaurant had to reduce its dining capacity from 100 to 60 patrons because of a government order. For this period, Linda qualifies for the ERC because she can prove this order caused a 10 percent or greater reduction in the restaurant’s “ability” to service customers.13

Supply Chain Disruption

It could be that what caused your 2020 or 2021 business trouble was a COVID-19 local, state, or federal government order that affected your suppliers instead of you directly.14

Example. You operate an auto parts manufacturing business. Because of a COVID-19 government order, your U.S.- based raw materials supplier was shut down. During this period, you had to cut back on your operations and per the IRS you would qualify for the ERC.15

Key point. In its example, the IRS declares you eligible. But don’t assume that’s so. Instead, create proof that you qualify because of either the 10 percent nominal effect or the 10 percent inability to provide goods and services in the normal course of your business.

Takeaways

If you operated a business during the COVID-19 epidemic, the government had various programs to help you. The ERC is just one of them.

But the ERC was overshadowed by other government programs, which contributed to the failure of many deserving businesses to apply for the ERC. And that’s the main point of this article: it’s not too late, even now in 2023, to amend your 2020 and 2021 payroll tax returns to claim your ERC.

Don’t procrastinate. The clock is ticking on the ability to claim the 2020 ERC. You need to make your claim no later than April 15, 2024—that’s only a little over 10 months away.

The path of least complication and biggest rewards is to qualify for the ERC under the decline-in-gross-receipts tests discussed in this article.

If you can’t qualify with the favorable gross receipts, options available to you include

· the 10 percent nominal-effect safe harbor, based on 2019 gross receipts or hours of service;

the 10 percent inability to provide goods and services (also a safe harbor, but more difficult to determine); and

· your specific facts and circumstances.